Debt from India, Indonesia, Brazil and South Africa has outperformed EM peers since April 2, when US President Donald Trump shocked global markets with his tariffs. The dollar rose in the four previous instances since 2021, when 10-year emerging-market bonds reacted to a rise in US benchmark yields. This time, however, the dollar has fallen, allowing currency returns to compensate for the duration spillover impact from higher US yields.

“Spillovers from rising US back-end rates to EM rates might be lower this time around” due to the effect of the weakening greenback, Goldman Sachs Group Inc. strategists including Kamakshya Trivedi and Danny Suwanapruti, wrote in a recent note. Higher-yielding EM bonds will tend to benefit more from this environment, they added.

AdPorts and Special Economic Zone has secured Rs 5,000 crore through a 15-year Non-Convertible Debenture. The issue was fully subscribed by LIC at a competitive rate. This move enhances APSEZ’s debt maturity profile. The proceeds will fund a proposed buyback of US Dollar bonds. APSEZ aims to handle 1 billion tonnes of cargo by 2029-30.

Bloomberg

BloombergDollar-funded investments into yielder EM bonds tend to be unhedged due to the high cost of implementing protection relative to their lower-yielding peers, and see larger FX gains when the dollar falls.

Live Events

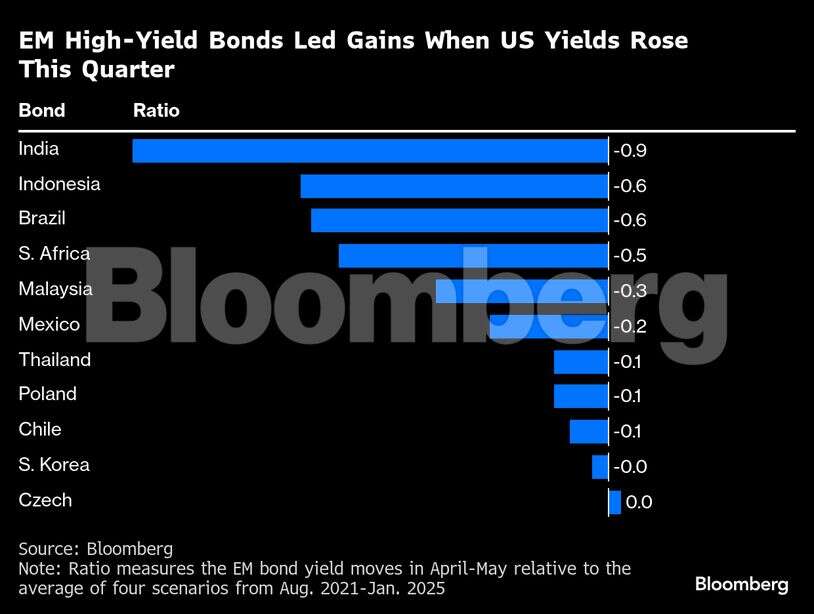

The ratio of yield moves this quarter versus the historical average for India was minus 0.88, versus Indonesia, Brazil and South Africa at -0.57, -0.55 and -0.50 respectively. This means that India’s yields in the most recent scenario have declined the most relative to its historical mean. Peers which offer lower yields, such as the Czech Republic and South Korea, tend to be more affected by the surge in US yields due to the tighter spreads.

“EM local markets have been a beneficiary of the weaker US dollar this year,” said Anders Faergemann, head of global sovereigns and economics at PineBridge Investments. “A continuation of that trend would help to cushion local bond performance.”

Bloomberg

Bloomberg